/

7 mins read

TL;DR

Most banking app teams measure the wrong finish line. KYC (Know Your Customer) completion looks like a win on a dashboard, but it predicts nothing about revenue, the metric that matters is the funded-account rate, and the drop-off between KYC_passed and account_funded is where most teams are silently losing conversions they've already paid to acquire. The best practices for onboarding new users in banking apps covered in this article address that gap directly: a five-stage event taxonomy (signup_started → KYC_started → KYC_passed → account_funded → first_value_action), a compliant in-app guidance playbook that intervenes at each drop-off point without touching regulated workflows, and a four-week implementation roadmap that gets measurable lift without engineering dependency. Teams implementing this framework typically see a 15–30% lift in funded-account rates and a 40–60% reduction in support tickets within the first 30 days.

Banking app teams don't lose funded-account conversions because the product is broken. They lose them because identity verification screens give users no recovery path when a document fails, funding screens assume intent without guiding action, and nobody is tracking what happens between KYC passing and an account getting funded.

Applying the best practices for onboarding new users in banking apps isn't primarily a compliance problem. It's an activation problem that happens to operate inside compliance constraints — and the two require completely different playbooks. Most teams optimize for passing regulatory checkpoints. The teams that win on funded-account conversion optimize for what users experience at each friction point along the way.

This article gives you three things: a five-stage event taxonomy you can instrument without a sprint, a compliant in-app guidance playbook that places contextual help at exactly the moments users stall, and a four-week roadmap for getting from baseline measurement to measurable lift. Teams using contextual in-app guidance at KYC friction points report 40–60% fewer support tickets in the first month. That number is a byproduct of fixing conversion, not a goal in itself.

The frame for everything that follows is this: onboarding doesn't end when KYC passes. It ends when a user funds an account and completes their first meaningful action. Everything before that is just setup.

Why banking app onboarding fails before the account Is Funded

KYC completion isn't the problem. The problem is that most teams treat it like the finish line.

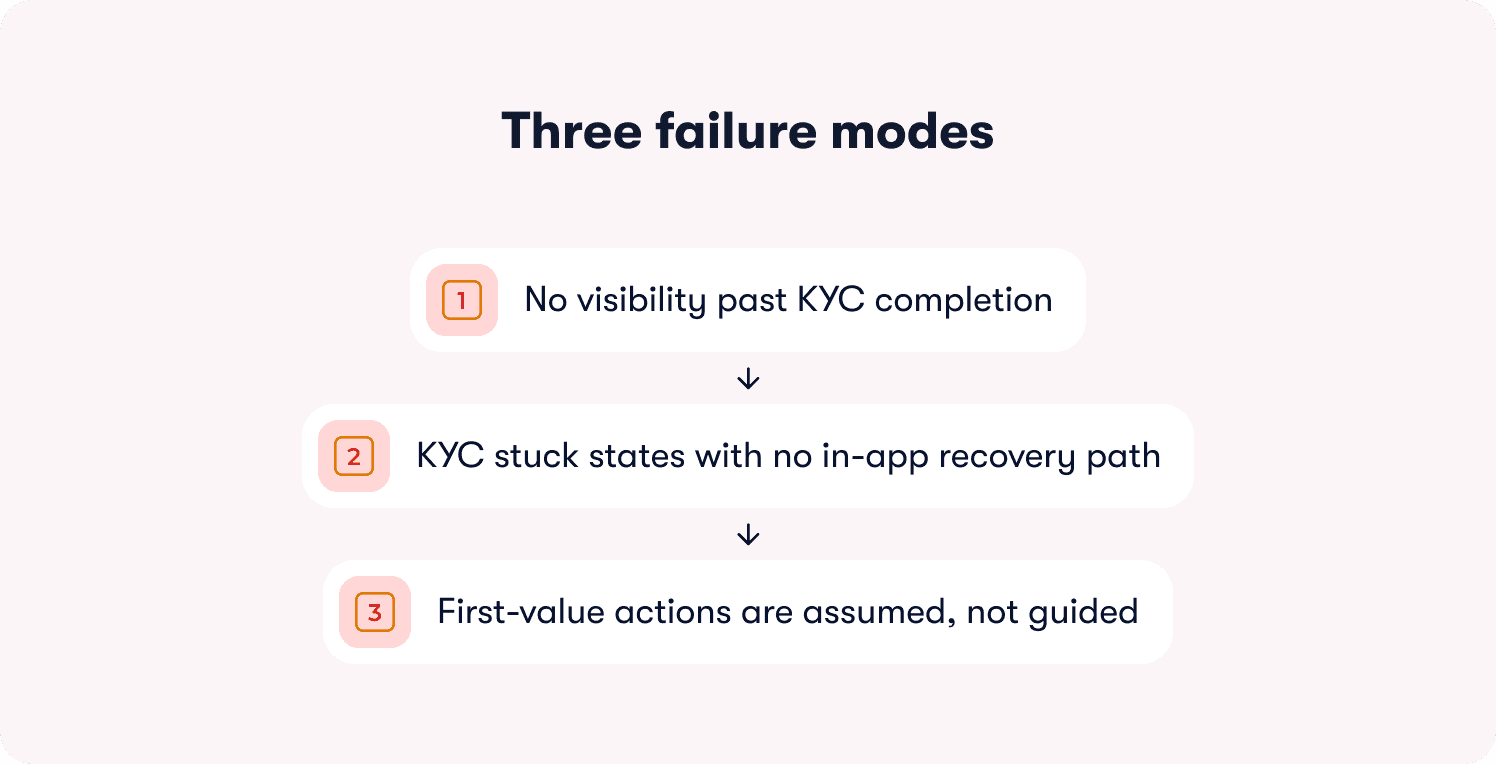

Three failure modes account for the majority of funded-account drop-off in banking apps. Each one is invisible until you instrument for it, and each one has a direct cost that shows up in revenue, not just UX scores.

Failure Mode 1: No visibility past KYC completion

Most product teams can tell you their signup rate and their KYC pass rate. Ask them what happens between KYC_passed and account_funded, and the answer is usually silence, or worse, a shrug toward "we assume most users complete it." That assumption is where the conversion gap hides. Without event tracking between those two states, there's no drop-off to investigate, no intervention to build, and no way to quantify what fixing it is worth. The funnel looks healthy right up until the cohort report lands.

Failure Mode 2: KYC stuck states with no in-app recovery path

A user uploads a blurry photo ID at 11pm. The submission fails. There's no hint explaining accepted formats, no tooltip surfacing a retry path, no contextual message telling them what went wrong or how to fix it. They close the app. They don't come back. That account was one well-placed contextual hint away from converting, and it cost the same to acquire as every other user in that cohort. The support ticket that follows — if it comes at all — arrives too late to save the conversion.

Failure Mode 3: First-value actions are assumed, not guided

Passing KYC is not activation. A user who verifies their identity but never makes a first deposit, sets up a first bill payment, or completes a first transfer has not been onboarded. They've been processed. Most banking apps draw a hard line at KYC completion because that's what compliance required, and the product experience stops there too. Users who cross that line but never reach a first-value action churn silently. They don't file a complaint. They don't submit a ticket. They just never come back, and nobody notices until the monthly cohort report shows a retention hole with no obvious cause.

The throughline across all three failures is the same: teams are measuring activity at the wrong stage, and building their interventions around the wrong outcome. KYC completion is a compliance milestone. Funded accounts are a revenue milestone. Closing the gap between them is an activation problem, and it starts with knowing exactly where users stop.

The onboarding measurement blueprint for banking apps

Every best practice in this article depends on one precondition: knowing exactly where users drop off. Without that, every guidance intervention is a guess. You're placing tooltips based on intuition, building checklists based on assumptions, and reporting on KYC completion rates that tell leadership nothing about whether the product is converting signups into revenue.

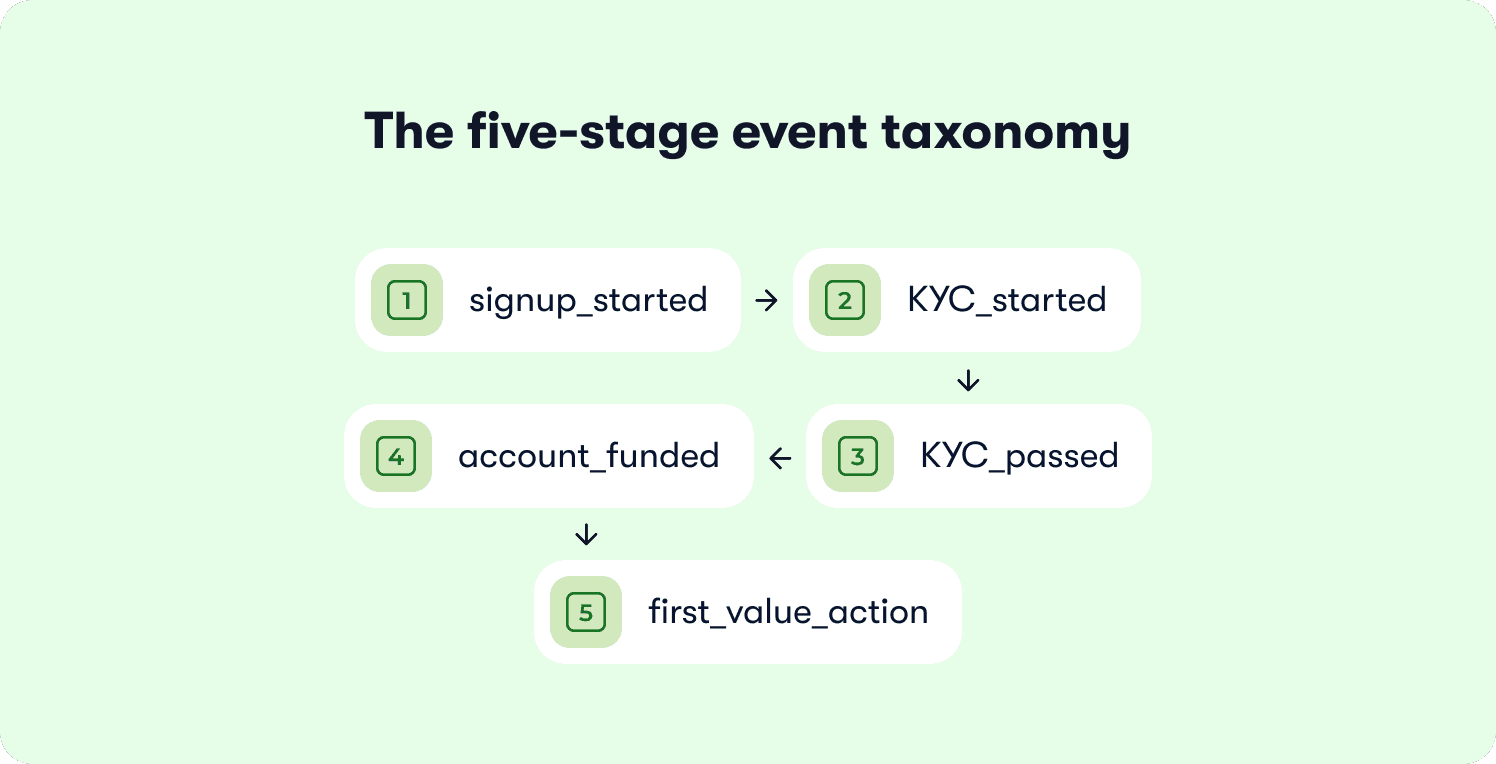

The five-stage event taxonomy below gives you the instrumentation foundation. It's designed to be handed to your product ops team and live in your analytics stack within a week, with no engineering dependency required.

Stage 1: signup_started. The user has initiated account creation. This is your acquisition baseline. Track it, but don't mistake volume here for health. A high signup_started rate with low KYC_started completion signals a friction point between registration and identity verification, usually a form length or flow structure issue.

Stage 2: KYC_started. The user has entered the identity verification flow. Drop-off between signup_started and KYC_started is typically a trust or friction problem: the product hasn't earned enough confidence for the user to hand over personal documents, or the entry into KYC is buried or poorly explained. This stage needs a contextual prompt that tells users why verification is required and what to expect on the other side.

Stage 3: KYC_passed. The user has cleared identity verification. This is the stage most teams celebrate. It shouldn't be. KYC_passed is not activation. It's clearance. The real conversion question starts here.

Stage 4: account_funded. The user has connected a funding source and completed a first deposit. This is the first genuine revenue signal. Drop-off between KYC_passed and account_funded is the most expensive gap in most banking app funnels, and it's almost always caused by the same thing: no guidance at the funding screen. Users who passed KYC have demonstrated intent. The product needs to meet that intent with a clear, guided path to the next action.

Stage 5: first_value_action. The user has completed a first deposit, first bill payment, or first transfer. This is activation. Not KYC. Not a funded balance sitting idle. An active account doing the thing it was opened to do. Users who reach this stage retain at dramatically higher rates. Users who don't, churn quietly, often within the first two weeks.

Each stage connects to an intervention. Significant drop-off between KYC_started and KYC_passed signals a guidance gap at the verification friction points — that's Best Practice 2. Significant drop-off between KYC_passed and account_funded signals a checklist gap at the funding screen — that's Best Practice 5. The measurement blueprint doesn't just describe the funnel. It tells you which section of this article to act on first.

The other critical point here is instrumentation speed. A VP of PLG who needs an engineering sprint to tag five events will be waiting three weeks before they have any baseline data to work with. Jimo's Success Tracker lets you define and tag custom activation events through a visual interface, clicking elements directly in your product without touching the codebase. Your team can have all five stages instrumented and a baseline established before the next sprint even starts.

Measurement is not the destination. It's the precondition for every intervention that follows.

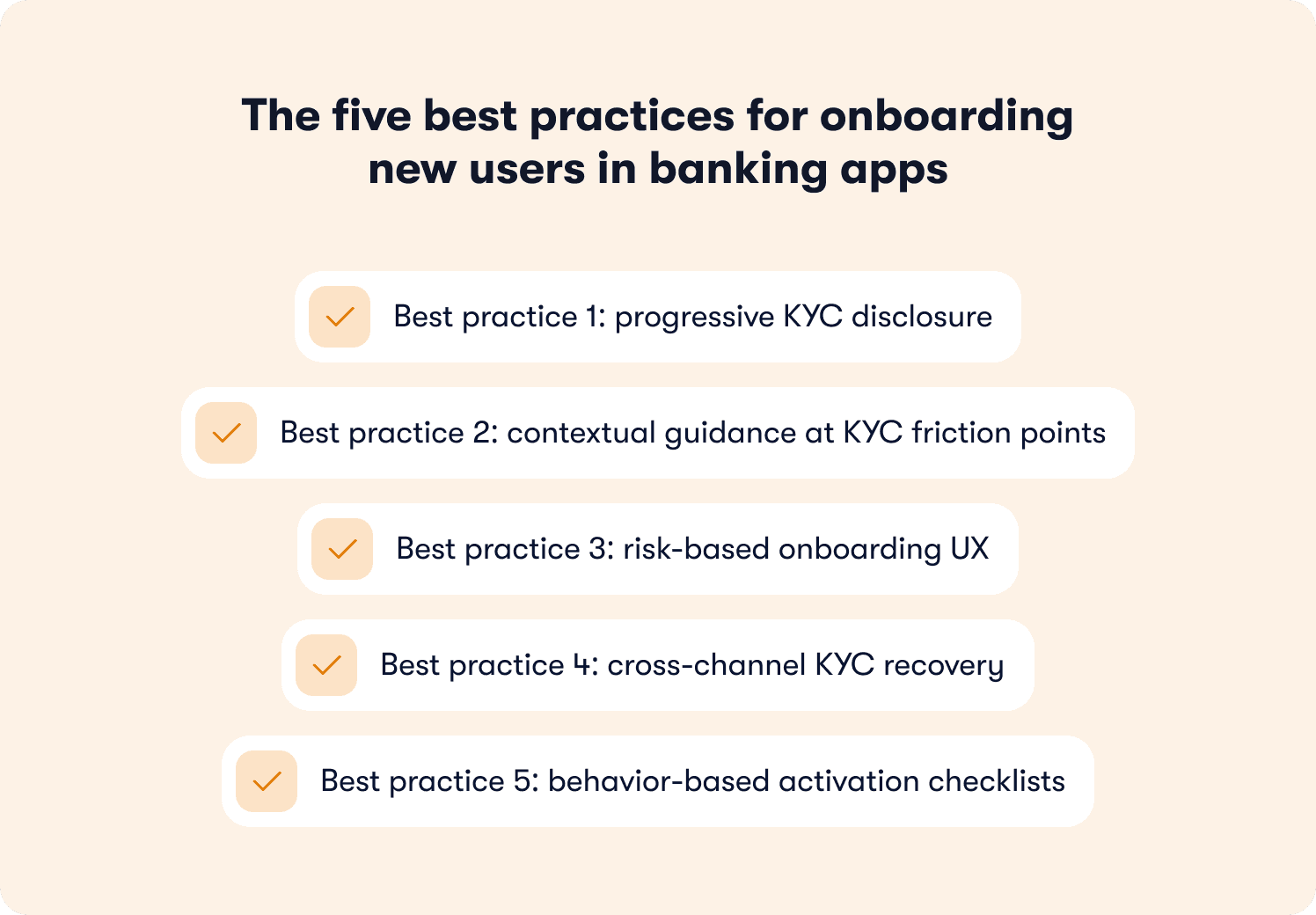

The five best practices for onboarding new users in banking apps

The measurement blueprint tells you where users drop off. These five best practices tell you what to build at each stage to stop it happening.

They're ordered to match the funnel. Start with your highest drop-off point from the baseline data, deploy the corresponding intervention, and measure lift before moving to the next. Teams that fix one stage at a time see funded-account improvement faster than teams that try to overhaul the entire flow at once.

One point worth stating before diving in: none of these practices require modifying a regulated workflow. Jimo deploys as a product-layer overlay, which means every guidance intervention sits above the KYC and AML flows. The compliance team reviews copy, not code. That distinction matters if you've previously been told the KYC flow is off-limits.

Best practice 1: progressive KYC disclosure

Front-loading every verification requirement at signup is the fastest way to kill conversion before it starts. Users who hit a document wall on step one don't think "this is thorough." They abandon — and these aren't bad-fit users. They're your highest-intent signups.

The fix is risk-tiered progressive disclosure: show users only what they need to provide right now.

Low-risk users: email + basic ID. Get them to a funded account fast.

Medium-risk users: full ID and address verification, split across two steps, each with a plain-language explanation of why it's required.

High-risk users: full KYC with a proactive live support offer at every step. Make it feel guided, not bureaucratic.

Jimo's analytics segments let you deploy different guidance flows for each tier without an engineering ticket. The compliance layer stays untouched. The user experience doesn't.

Best practice 2: contextual guidance at KYC friction points

KYC doesn't fail because users don't want to complete it. It fails because the product goes silent exactly when users need help most. Four screens drive the majority of abandonment.

ID upload screen: A contextual hint triggered after 45 seconds of inactivity, surfacing accepted formats and a link to a 30-second walkthrough. One tooltip. No modal.

Address entry field: An inline tooltip on the third edit of the same field, showing the expected format with a one-line example. Auto-dismiss once correctly formatted.

Document quality check: A step-by-step walkthrough triggered immediately after a failed submission, covering the three most common quality issues. Under four steps, ending with a retry CTA.

Funding screen: A behavior-triggered checklist step surfaced after KYC_passed, with a direct CTA and one-sentence explanation of what happens next.

Guidance sits alongside regulated workflows, never inside them. Teams deploying contextual hints at KYC friction points report 40–60% fewer support tickets in the first month.

Best practice 3: risk-based onboarding UX

Not every user needs the same path. The mistake most teams make is routing everyone through full KYC regardless of their actual risk profile, generating friction for low-risk users that has no compliance benefit and a direct conversion cost.

The decision tree is straightforward:

Low-risk path: Minimal verification, fast track to first value. No unnecessary steps, no document requests the risk profile doesn't warrant.

Medium-risk path: Step-up verification with a plain-language explanation at each additional requirement. Users who understand why they're being asked for something comply at significantly higher rates than users who hit unexplained form fields.

High-risk path: Full KYC with a proactive live support offer at each step. These users expect the process to be thorough. The job is to make it feel guided.

The PLG framing here matters: this is not a compliance decision, it's a conversion decision. Every low-risk user routed through full KYC is a funded-account conversion you've made harder than it needed to be. Jimo's behavior metrics surface exactly which path each user segment is taking and where they're dropping off, so you can identify false-positive friction before it shows up in the monthly cohort report.

Best practice 4: cross-channel KYC recovery

Every KYC stuck state has a recovery path. The teams that don't build them are leaving re-engageable users on the table — users who have already invested time in verification and are one well-timed nudge away from completing it.

Map your top failure reasons to specific recovery channels:

Blurry ID photo: In-app hint with accepted format examples, triggered immediately on failed submission.

Missing document: Push notification two hours after failure if not resolved in-app, with a direct link back to the stuck step.

Address mismatch: SMS with a correction link and a one-sentence explanation of the issue.

Session timeout mid-KYC: Email with a deep link back to the exact stage where the user stopped, not the start of the flow.

The timing matters as much as the channel. A recovery nudge sent 24 hours after a stuck state converts at a fraction of the rate of one sent within two hours. Jimo's retention insights show you which stuck states are most common and which recovery interventions are pulling users back, so you're iterating on data rather than assumptions.

Re-engaging a user who stalled mid-KYC costs a fraction of acquiring a new one. Build the recovery flows before you go looking for more top-of-funnel volume.

Best practice 5: behavior-based activation checklists

A user who clicks through a setup wizard has completed a task. A user who makes a first deposit has been activated. Only one of those predicts retention.

Most banking app checklists are built around the wrong outcome. "Upload your profile photo" and "Complete your account details" are process tasks, not activation events. They give users something to check off without moving the metric that matters.

Replace them with behavior-driven items where completion is triggered by the actual action, not by a click:

Identity verified ✓ (triggered by KYC_passed)

Funding source connected ✓ (triggered by bank_linked)

First deposit made ✓ (triggered by account_funded)

First transaction completed ✓ (triggered by first_value_action)

Notifications enabled ✓ (triggered by notifications_on)

Each item links directly to a guided walkthrough so users aren't just reminded what to do — they're walked through doing it. That distinction is where the 15–30% funded-account lift comes from. Teams that replace profile-completion checklists with behavior-based ones close the gap between KYC_passed and account_funded faster than any other single intervention in the playbook.

Jimo's onboarding checklists connect each task to an interactive tour, so the checklist is an activation engine, not a to-do list.

How to measure what actually predicts funded-account revenue

KYC completion rate is not a revenue metric nor a tour completion rate. Neither is DAU. These numbers look good in a weekly report and tell you almost nothing about whether the product is converting signups into funded, active accounts.

Three metrics predict revenue. Everything else is context.

KYC completion rate: Conversion from KYC_started to KYC_passed. The baseline health check for your verification flow. If this is below 70%, the problem is friction inside the KYC process itself, and Best Practices 1 and 2 are where to start.

Funded-account rate: Conversion from KYC_passed to account_funded. This is the metric most teams aren't measuring, and it's where the majority of revenue is leaking. A 10 percentage point improvement here has a direct, attributable impact on monthly revenue that a VP of PLG can put in front of a board.

Time-to-first-value: Time elapsed between account_funded and first_value_action. Users who complete a first deposit but sit idle for more than 72 hours churn at significantly higher rates than users who transact within the first day. Speed to first value is a retention predictor, not just an onboarding metric.

The dashboard that connects these three isn't complicated. Drop-off between KYC_started and KYC_passed points to Best Practices 1 and 2. Drop-off between KYC_passed and account_funded points to Best Practice 5. A long time-to-first-value points to a gap in post-funding guidance that none of the five practices above have addressed yet.

A VP of PLG who can show "we deployed in-app guidance at the funding screen and funded-account rate increased 22% in 30 days" has a business case. One who can only show "KYC completion was up 8%" does not. Jimo's actionable reports connect guidance interventions directly to each of these three outcome metrics, so the ROI narrative builds itself.

Implementation roadmap: four weeks to measurable lift

This is not a transformation project. It's a four-week sprint with a clear deliverable at the end of each week and a measurable outcome by day 28. Hand this to your product ops team on Monday and the first intervention can be live by Friday.

Week 1: Instrument the event taxonomy. Tag all five stages — signup_started, KYC_started, KYC_passed, account_funded, first_value_action — using visual tagging. No engineering tickets. By end of week, you have baseline conversion rates for every stage and a clear picture of where the biggest drop-off sits.

Week 2: Deploy one intervention at the highest drop-off stage. One guidance intervention, not five. A hint at the ID upload screen, a checklist step at the funding screen, a recovery push notification for stuck KYC states at whichever stage is losing the most users. Launch to 20% of new users as an A/B test against the unguided control group.

Week 3: Measure and expand. If funded-account rate improves by more than five percentage points against the control, expand to 100% of new users. If not, adjust the guidance format or timing and re-test. The point of Week 3 is not to declare victory. It's to iterate fast enough that Week 4 starts from a stronger baseline.

Week 4: Add the behavior-based checklist and recovery flows. With the single biggest drop-off addressed, build the full activation checklist and map your top two KYC stuck states to cross-channel recovery sequences. Connect checklist completion events to your analytics stack and establish the three revenue metrics: KYC completion rate, funded-account rate, time-to-first-value as the standing dashboard your team reports against.

Four weeks. One sprint. A funded-account rate your cohort reports will actually reflect. See how teams build product-led expansion in banking with Jimo.

FAQs

What is client onboarding in banking?

Client onboarding in banking is the process of converting a signup into a funded, active account: identity verification, compliance checks, funding source connection, and first-value action completion. The critical distinction most teams miss is that onboarding doesn't end at KYC completion. It ends when the user makes their first deposit or transaction. Everything before that is setup, not activation.

What does a banking client onboarding process flow chart include?

The five stages that matter for revenue: signup_started → KYC_started → KYC_passed → account_funded → first_value_action. For each stage: the event to track, the most common drop-off reason, and the intervention type that addresses it. This taxonomy is the foundation for every measurement and guidance decision in this article.

Where can I find a client onboarding template for banking apps?

Jimo's onboarding event taxonomy template includes pre-defined events, drop-off benchmarks, and guidance placement recommendations for each funnel stage. It's built specifically for banking and fintech teams instrumenting their first activation funnel. Download the template here.

How does client onboarding in financial services differ from other SaaS products?

The compliance constraint changes everything. Banking onboarding must satisfy KYC and AML requirements while still optimizing for conversion — and guidance must sit alongside regulated workflows, not inside them. Risk-based UX and behavior-triggered contextual guidance are the tools that solve this without touching the compliance layer. Most generic onboarding playbooks don't account for this boundary, which is why banking teams need a vertical-specific approach.

What is digital onboarding in banking?

Self-serve account creation and identity verification completed entirely in-app, without branch visits or manual document submission. The activation goal is a funded account with a completed first-value action — not a verified identity. Teams that define digital onboarding success as KYC completion are measuring the wrong finish line.